How Much Is ABA Therapy Out of Pocket?

Navigate ABA therapy costs with ease! Discover how much is out of pocket and explore financial assistance options.

Understanding ABA Therapy Costs

ABA therapy, or Applied Behavior Analysis therapy, is an evidence-based treatment for individuals with autism spectrum disorder (ASD). It aims to improve social, communication, and behavioral skills. However, the costs associated with ABA therapy can vary significantly. In this section, we will provide an overview of ABA therapy costs and explore the factors that influence them.

ABA Therapy Cost Overview

The cost of ABA therapy can be a significant concern for families seeking treatment for their loved ones. Without insurance coverage, the annual costs of ABA therapy can range from $62,400 to $249,600, with monthly costs ranging from $4,800 to over $20,000 [1]. Weekly costs can start at $1,200 and go up to $4,800 without insurance coverage.

The cost of ABA therapy is typically calculated based on the number of therapy hours provided. In the United States, ABA therapy with a board-certified ABA therapist can cost approximately $120 per hour. However, the number of therapy hours required can vary depending on the individual's needs and can range from 20 to 40 hours per week.

It's important to note that the lifetime costs of autism treatment can be substantial. In 2015, the average lifetime cost for a person with autism and intellectual disability was $2.4 million, while for individuals with autism without intellectual disability, it averaged $1.4 million. These figures encompass various aspects of autism treatment, including ABA therapy.

Factors Influencing ABA Costs

Several factors contribute to the overall costs of ABA therapy. These factors can vary depending on individual circumstances and location. Some of the key factors influencing ABA therapy costs include:

- Therapy Hours: The number of therapy hours required per week significantly impacts the cost of ABA therapy. Children with more intensive needs may require more therapy hours, leading to higher costs.

- Therapist Qualifications: The qualifications and experience of the ABA therapist can influence the cost of therapy. Board-certified ABA therapists typically charge higher rates due to their specialized training.

- Geographical Location: The cost of living and regional rates for therapy services can vary depending on the location. Urban areas, for example, tend to have higher therapy costs compared to rural areas.

- Insurance Coverage: Insurance coverage plays a crucial role in determining the out-of-pocket expenses for ABA therapy. With insurance coverage, the costs are significantly reduced, making therapy more accessible and affordable for families.

- Additional Services: Depending on the individual's needs, additional services such as speech therapy or occupational therapy may be recommended alongside ABA therapy. These additional services can contribute to the overall costs of treatment.

Understanding the cost overview and the factors that influence ABA therapy costs can help families navigate the financial considerations associated with this treatment. Insurance coverage, financial assistance programs, and exploring different payment strategies can help alleviate the financial burden, ensuring that individuals with autism have access to the necessary therapies.

Insurance Coverage for ABA Therapy

When it comes to covering the costs of Applied Behavior Analysis (ABA) therapy, insurance can play a significant role. Understanding the criteria for insurance coverage and the types of coverage available is essential for families seeking ABA therapy for their loved ones.

Insurance Criteria for ABA Coverage

Most insurance companies only cover ABA therapy with an Autism diagnosis. In some cases, insurance carriers may require a letter from the treating physician, stating the medical necessity of ABA therapy. The specific criteria for coverage can vary between insurance providers, so it's crucial to review your policy or contact your insurance company directly to understand the requirements.

Types of Insurance Coverage

Insurance coverage for ABA therapy varies depending on the provider and the type of therapy covered, whether it's in-home or center-based. Many private insurance providers offer coverage for autism therapy, including ABA therapy and autism evaluations. However, the level of coverage and limitations can differ. Some insurance plans have a maximum amount of coverage per year after meeting the deductible, while others may offer a limited number of fee-free therapy sessions [4].

It's important to note that insurance coverage for ABA therapy is mandated by insurance companies in several states to cover autism treatment costs. This means that parents may only need to pay the agreed deductible, making the sessions more affordable compared to paying out of pocket.

Understanding the coverage provided by your insurance plan and any limitations or requirements is crucial to ensure that the costs of ABA therapy are covered as much as possible. It is recommended to contact your insurance provider directly to review your policy and clarify the coverage for ABA therapy.

By exploring the insurance criteria for ABA coverage and understanding the types of insurance coverage available, families can better navigate the financial aspects of ABA therapy and ensure that their loved ones receive the necessary treatment without incurring excessive out-of-pocket expenses.

Financial Assistance Options

When it comes to covering the costs of ABA therapy, there are various financial assistance options available for families. These options can help alleviate the financial burden and make ABA therapy more accessible. Here are three common financial assistance options to consider:

Autism Grants and Programs

Several grants and programs are specifically designed to provide financial assistance to families seeking ABA therapy for their children with autism. These grants are typically offered by organizations and foundations that aim to support individuals with autism and their families.

- Autism Care Today's Quarterly Assistance Program offers direct financial help to families who may not be able to afford services like ABA therapy on their own.

- Special Angels Foundation provides grants for obtaining therapies, including ABA therapy, based on specific criteria and medical verification.

- The CARE Family Grant Program assists families with expenses related to therapy sessions, including ABA therapy, by providing grants that are paid directly to the service provider.

- The United Healthcare Children's Foundation (UHCCF) offers financial assistance to families with children who have medical needs not fully covered by their commercial health insurance plan, including coverage for ABA therapy [5].

- MyGOAL Autism Grant Program provides yearly grants to support and care for individuals with autism under 18 years old, covering treatments, enrichment, and educational needs, including ABA therapy that may not be covered by other funding sources or insurance.

Health Savings Account (HSA) Funds

Health Savings Accounts (HSAs) are tax-advantaged accounts that allow individuals to set aside funds for qualified medical expenses. These accounts can be used to cover various healthcare costs, including ABA therapy. Contributions to HSAs are tax-deductible, and any unused funds can be rolled over from year to year.

If you have an HSA, you can use the funds to pay for ABA therapy expenses for yourself, your spouse, or your dependents. It's important to note that ABA therapy must be considered a qualified medical expense according to the guidelines set by the Internal Revenue Service (IRS). Consult with a tax professional or refer to the IRS guidelines for more information on eligible expenses.

Medicare and Medicaid Coverage

Medicare and Medicaid are federal healthcare programs that provide coverage for eligible individuals, including children and adults with autism who require ABA therapy. The coverage and eligibility criteria may vary depending on the state and the specific program.

Medicare, which primarily serves individuals aged 65 and older, may cover ABA therapy for children with autism under certain circumstances, such as if the therapy is deemed medically necessary. It's important to consult with Medicare and your healthcare provider to determine the specific coverage options.

Medicaid, on the other hand, provides coverage for low-income individuals and families. Medicaid coverage for ABA therapy varies by state, and some states have specific requirements and limitations. It's essential to contact your state's Medicaid program to understand the coverage criteria and process for accessing ABA therapy.

By exploring these financial assistance options, families can find support in covering the costs of ABA therapy. Whether through grants and programs, utilizing HSA funds, or accessing Medicare and Medicaid coverage, these resources can help make ABA therapy more affordable and accessible for individuals with autism.

Out-of-Pocket Payment Strategies

When it comes to covering the costs of ABA therapy, there are various out-of-pocket payment strategies that families can consider. These strategies can help alleviate the financial burden and ensure that children receive the necessary therapy. Three common out-of-pocket payment options include private payment, employer-based coverage, and school-funded ABA therapy.

Private Payment Options

Paying for ABA therapy privately through direct payments is an option that some families explore. While it may not be feasible for all families, it can provide the assurance that the child receives the necessary therapy. Some therapists may offer discounted rates for clients who make direct payments, potentially saving money in the long run for families who choose this option.

Employer-Based Coverage

Private payment options can also be linked to employers or work organizations. In some cases, employers may offer coverage or assistance for ABA therapy expenses as part of their employee benefits. This can significantly reduce the financial burden for families. Depending on individual circumstances, this method can potentially reduce expenses by over 80%.

School-Funded ABA Therapy

Another potential option for families is school-funded ABA therapy. This option involves the child's school or school district covering 100% of the therapy costs, provided the application is approved. The therapy sessions are conducted by therapists who are supervised by Board Certified Behavior Analysts or Board Certified Assistant Behavior Analysts. School-funded ABA therapy can be a valuable resource for families and help alleviate the financial burden associated with therapy expenses.

It's important to note that the availability of these out-of-pocket payment strategies may vary depending on individual circumstances, geographical location, and the specific resources available. Families should explore all available options, including private payment, employer-based coverage, and school-funded ABA therapy, to determine the most suitable strategy for their situation. Seeking guidance from professionals and utilizing financial assistance programs can also provide additional support in navigating the costs of ABA therapy.

Cost Disparities in Healthcare Systems

When it comes to accessing ABA therapy for individuals with autism spectrum disorder (ASD), there are notable cost disparities between Medicaid and private insurance. Understanding these differences is crucial for families seeking ABA therapy and managing out-of-pocket expenses. Additionally, comparing the costs of different services can provide further insights into the financial aspects of ABA therapy.

Medicaid vs. Private Insurance

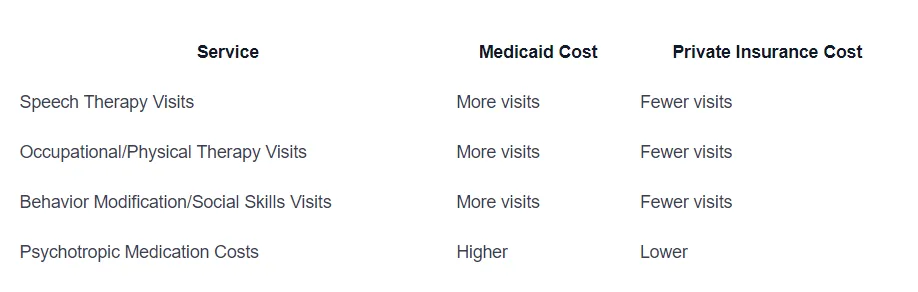

Research has shown significant variations in healthcare costs between Medicaid and private insurance for children with ASD. In terms of costs and service use per child with ASD, Medicaid had higher total healthcare costs, higher ASD-specific costs, higher psychotropic medication costs, more speech therapy visits, more occupational/physical therapy visits, and more behavior modification/social skills visits compared to private insurance.

- Average total healthcare costs per child with ASD were more than four times higher in Medicaid than in private insurance.

- The biggest component of the cost difference across Medicaid and private insurance was in outpatient services.

- Psychiatric care costs for ASD were over five times higher in Medicaid than in private insurance and were responsible for a larger fraction of total healthcare costs per child with ASD.

- ASD-specific service costs were eight times higher in Medicaid than in the private sector.

These findings highlight the financial disparities between Medicaid and private insurance when it comes to accessing ABA therapy and related services for children with ASD.

Service Costs Comparison

Comparing the costs of different services within ABA therapy can provide further insights into the financial aspects of treatment. The costs associated with ABA therapy can vary based on the specific services provided. Here is a general comparison of some common ABA therapy service costs:

These cost comparisons demonstrate the variations in service costs between Medicaid and private insurance. It is important for families to consider these differences when assessing the financial implications of ABA therapy and making informed decisions about coverage and payment options.

Understanding the cost disparities in healthcare systems and the differences in service costs can help families navigate the financial aspects of ABA therapy. Exploring available insurance coverage options, financial assistance programs, and additional support resources can provide further assistance in managing the out-of-pocket expenses associated with ABA therapy for individuals with ASD.

Additional Financial Support Resources

In addition to insurance coverage and out-of-pocket payment strategies, there are several additional financial support resources available to assist individuals and families with the costs of ABA therapy. These resources can help alleviate the financial burden and provide access to necessary services. Here are three key resources to consider:

ABLE Accounts

The ABLE Act of 2014 authorized the establishment of private tax-advantaged savings accounts, known as ABLE accounts. These accounts are designed to help families of individuals with disabilities save for long-term expenses without impacting eligibility for public benefits such as Medicaid and Supplemental Security Income (SSI). Each state is responsible for establishing and operating an ABLE program, and as of April 2016, over 40 states have enacted ABLE laws.

ABLE accounts provide individuals with disabilities, including those with autism, the opportunity to save and invest money for qualified disability-related expenses. Some of the key benefits of ABLE accounts include tax advantages, asset protection, and the ability to maintain eligibility for essential public benefits. These accounts can be used to cover various expenses related to ABA therapy, such as therapy sessions, evaluations, and specialized equipment.

Medicaid Waivers

Medicaid Waivers, also known as 1915(c) Home and Community Based Services, are available in most states to provide support services and care for individuals with developmental disabilities, including autism. These waiver programs offer coverage for medical treatments, respite care, transportation, in-home support, and more. The specific services covered by Medicaid Waivers can vary by state, and eligibility criteria may also differ.

By accessing Medicaid Waivers, individuals with autism and their families can receive financial assistance to help cover the costs of ABA therapy. These waivers aim to support individuals in remaining at home or in the community, providing essential services that contribute to their overall well-being and development. It is important to check with your state's Medicaid program to understand the specific waiver programs available and the requirements for eligibility.

Social Security Benefits

For individuals with autism who meet the eligibility criteria, Social Security benefits can provide additional financial support. Two key benefits to consider are Supplemental Security Income (SSI) and Social Security Disability Insurance (SSDI).

Supplemental Security Income (SSI) is a monthly government payment through Social Security designed to support individuals who are aged (65 and older), blind, or disabled. Individuals with autism may be eligible to receive SSI for financial support. More information about SSI and how to apply can be found at www.ssa.gov.

Social Security Disability Insurance (SSDI) is another financial benefit available through Social Security for disabled adults. SSDI can be considered a "child's" benefit because it is paid based on a parent's Social Security earnings record. Individuals can qualify for SSDI if they are disabled at age 18, among other criteria. More details about SSDI can be found in the booklet "Benefits for Children with Disabilities".

Exploring these additional financial support resources can significantly assist individuals and families in managing the costs of ABA therapy. Each resource offers unique opportunities and benefits, so it is important to research and understand the specific eligibility criteria and guidelines to make informed decisions regarding financial assistance.

References

- https://www.crossrivertherapy.com/insurance

- https://www.autismparentingmagazine.com/aba-therapy-autism-cost/

- https://www.myteamaba.com/resources/cost-of-autism-treatment

- https://www.songbirdcare.com/articles/how-much-does-aba-therapy-cost

- https://www.autismspeaks.org/autism-grants-families

- https://www.songbirdcare.com/articles/aba-therapy-cost-per-state

- https://www.ncbi.nlm.nih.gov/pmc/articles/PMC3534815/

- https://www.autismspeaks.org/financial-autism-support

Does Your Child Have An Autism Diagnosis?

Learn More About How ABA Therapy Can Help

Find More Articles

How Autism Affects Your Social Battery and Recharging Tips

Creative Writing for Autistic Individuals: Tips & Techniques

Special Needs Trusts for Autism: A Guide

Nail Biting in Autism: Causes, Effects, and Coping Strategies

Autism and Attachment Styles in Children with ASD

10 Autism-Friendly Activities in and Around Charlotte, NC

Autism in Charlotte: What the Numbers Reveal (2025)

Teaching coping strategies with ABA

Using ABA to improve attention to task

What is response blocking in ABA

How to support children with anxiety using behavior strategies

How to write effective behavior goals

The role of data collection in ABA decision-making

How to teach goal-setting to older children

How to teach turn-taking using ABA

How to identify triggers for challenging behavior

Understanding prompt hierarchy in ABA

Common myths about ABA therapy debunked

Behavioral strategies for addressing compulsive behavior

The science behind reinforcement in ABA therapy

ABA tips for co-regulation with caregivers

Teaching perspective-taking to children with autism

Teaching abstract concepts like time using ABA

Building independence in older autistic individuals

Strategies for working through therapy resistance

Do Amish Kids Get Autism? Are They Vaccinated?

Using ABA to teach vocational skills

How to use chaining to teach multi-step tasks

Can ABA therapy help with social skills development in teens

What are motivating operations in ABA

Teaching honesty and truthfulness through ABA

Tips for managing caregiver stress during ABA therapy

Can ABA support emotional regulation in autistic children

ABA strategies for addressing excessive reassurance-seeking

Supporting children during puberty with behavior supports

Using ABA to support bilingual or multilingual children

How to identify overly rigid behaviors

How to assess for progress beyond behavior

Tips for setting up your home for ABA success

How to support autistic children in group learning settings

Teaching effective help-seeking behavior

What is instructional control and why it matters

How therapists assess progress in ABA programs

What is behavioral contrast in ABA

How to build motivation for difficult tasks

Supporting attention span through ABA

Teaching context clues in social settings

Using ABA to help with sensory-seeking behaviors

Supporting transitions from therapy to school independently

How to support early learners in group ABA sessions

Using role-playing to teach social situations

Supporting generalization of academic skills

What to do when reinforcement stops working

What to expect during an ABA reassessment

Sensory-friendly spaces and their role in supporting autistic children

ABA approaches to reduce property destruction

ABA approaches to reducing impulsive behaviors

ABA strategies for building study habits

5 Autistic Child Traits by the Age of 3

Odds of Second Child Also Being Autistic

Odds Of Having A Child With Autism By Age

Does Living In A City Cause Autism?

Strengths and Abilities In Autism

Sensory Processing Disorder vs. Autism

Does Tilly Green Have Autism?

Which Parent Carries The Autism Gene?

What Is The Autism Society Of North Carolina?

Do Plastic Toys Cause Autism?

Autism Prevalence In North Carolina

Signs & Symptoms of Autism in Teens

Does Emotional Neglect Cause Autism?

Does The Good Doctor Have Autism?

Does Cerebral Palsy Cause Autism?

Does My Child Have Autism?

What Happens If Autism Is Not Treated?

Is it Worth Getting An Autism Diagnosis?

Do Autistic People Talk To Themselves?

Why Do Autistic People Like Trains?

Why Do Autistic People Wear Headphones?

Does My Boyfriend Have Autism?

Does My Boyfriend Have Autism?

What Is Action Behavior Centers?

Free ABA Therapy Services for My Child With Autism

What Happens To Severely Autistic Adults?

Can You Join The Military With Autism?

Is Your Autistic Adult Child Ready To Move Out?

Movies & TV Shows About Autism

Contact us

North Carolina, Nevada, Utah, Virginia

New Hampshire, Maine

Arizona, Colorado, Georgia, New Mexico, Oklahoma, Texas

.avif)